Most businesses don't realize they're overpaying for cross-border payments until they compare what left their account with what actually reached the beneficiary.

The transfer fee is only one part of the equation. FX markups, intermediary-bank deductions, failed payments, delayed settlement, and manual reconciliation often create a much larger cost than the payment fee itself.

The challenge is reducing those costs without making payments slower or introducing operational and compliance risks.

This guide explains practical ways to lower the total cost of international payments while maintaining reliable settlement, predictable delivery, and strong operational controls. Whether you're paying suppliers, contractors, subsidiaries, or marketplace sellers, these strategies will help you identify hidden costs and optimize every payment corridor.

Most payment providers advertise a transaction fee, but that number rarely reflects what an international payment actually costs.

By the time funds reach the beneficiary, businesses may also have absorbed currency conversion costs, intermediary-bank deductions, payment investigations, manual reconciliation work, and liquidity tied up during settlement. These expenses accumulate across hundreds or thousands of payments, making them far more significant than the visible transfer fee.

In practice, the total cost of an international payment often includes:

The G20 and Financial Stability Board identify four major challenges in cross-border payments: cost, speed, transparency, and access. Improving one while sacrificing the others rarely produces better outcomes. A cheaper payment route provides little value if it consistently creates delayed supplier payments, missing funds, compliance reviews, or reconciliation problems.

Before negotiating pricing with a provider, finance teams should identify every point in the payment journey where cost is introduced. Understanding the full economics of each corridor creates the foundation for meaningful optimization.

Reducing payment costs starts with visibility, not negotiation. Before comparing providers or changing payment routes, finance teams should understand where costs enter the payment lifecycle.

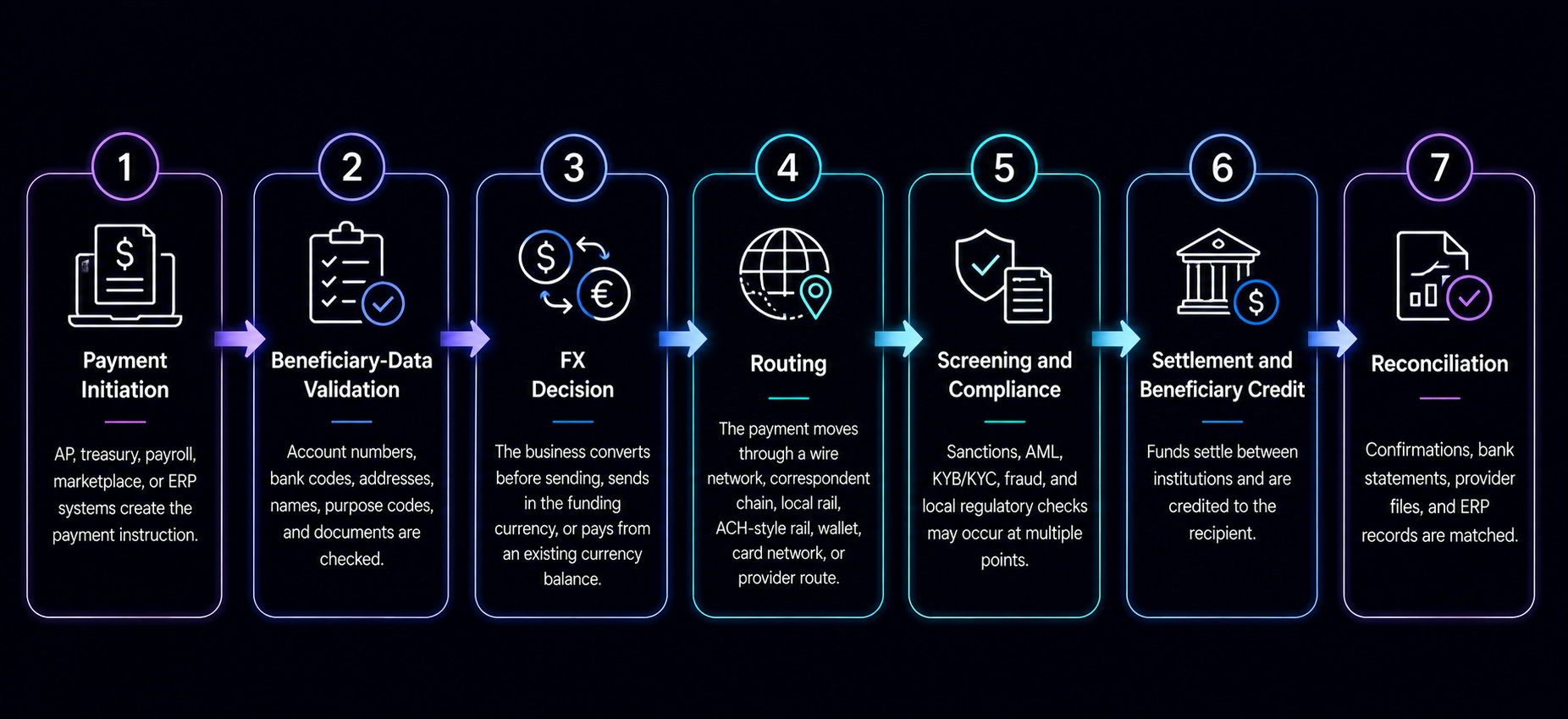

A typical cross-border payment journey includes seven steps.

For every major payment corridor, build a simple operating inventory that includes:

This information quickly highlights which corridors generate the highest operational cost. Without a corridor-level view, businesses often negotiate lower transfer fees while overlooking the larger expenses created by FX, delays, and payment exceptions.

Many businesses assume high payment costs are unavoidable. In reality, a significant portion of international payment expenses comes from inefficient processes rather than the payment itself.

One of the most common issues is FX leakage. A provider may advertise low transaction fees while applying a wide exchange-rate spread. On large international payments, the hidden FX cost can easily exceed the visible transfer fee.

Another frequent source of unnecessary expense is routing every payment the same way. Sending every supplier payment via an urgent international wire may improve speed, but it also increases costs for transfers that were never time-sensitive.

Businesses also lose money through fragmented payment operations. Processing invoices individually instead of batching payments increases banking fees, operational workload, and approval time. Likewise, maintaining idle prefunded balances across multiple providers ties up working capital that could be used elsewhere.

Poor beneficiary data creates another layer of avoidable cost. Incorrect bank details, missing regulatory information, or inconsistent beneficiary names often result in repair fees, returned payments, compliance reviews, and delayed settlement.

Finally, manual investigations and reconciliation consume more resources than many finance teams expect. Every failed payment requires additional coordination between treasury, finance, support teams, banking partners, and the recipient, increasing both direct and indirect costs.

Rather than treating every payment issue as an isolated incident, classify payment failures over a 30- to 90-day period. Patterns usually reveal whether costs are driven by FX pricing, data quality, routing decisions, provider coverage, or internal operational processes.

Reducing cross-border payment costs starts with measuring the right numbers. Looking only at transfer fees provides an incomplete picture because many of the largest expenses sit elsewhere in the payment process.

A practical way to evaluate international payments is to calculate the all-in cost for each payment corridor rather than relying on blended averages.

All-in cost per payment = Provider fee + FX spread cost + Intermediary or receiving-bank fees + Failed-payment cost + Internal operations cost + Liquidity cost

Each component should be measured consistently:

Evaluate each payment corridor independently. A USD-EUR supplier payment behaves very differently from a USD-PHP payroll transfer or a GBP-INR marketplace payout. Corridor-level analysis helps finance teams identify where the greatest savings can be achieved instead of relying on misleading global averages.

Simple percentage math like calculating transfer fees or savings gets easier with a quick tool like this Percentage Calculator, helping businesses compare payment methods more accurately.

The objective isn't simply to reduce transaction fees, it's to reduce the total cost of moving money internationally.

Not every international payment requires the fastest or most expensive settlement option. Applying the same payment method across every transaction often increases costs without improving business outcomes.

Instead, group payments based on their operational requirements and match each category with the most appropriate payment route.

A supplier invoice due tomorrow has very different priorities from a weekly contractor payout or a monthly marketplace disbursement. High-value treasury transfers typically prioritize settlement certainty and traceability, while recurring low-value payments benefit more from lower-cost routing and automation.

Common payment segments include:

Each segment should have its own routing policy based on urgency, payment value, recipient expectations, and compliance requirements.

For example, paying premium fees for same-day settlement rarely makes sense if next-day delivery fully meets contractual obligations. Likewise, selecting the cheapest payment route is not worthwhile if it increases failed payments, customer support requests, or reconciliation effort.

By defining a preferred and backup payment route for every major payment segment, finance teams can reduce costs while maintaining consistent operational performance across all payment corridors.

There is no single payment route that delivers the lowest cost across every corridor. The most efficient option depends on factors such as destination country, payment value, settlement urgency, beneficiary preference, and regulatory requirements.

Traditional SWIFT transfers remain the preferred choice for many high-value international payments because of their global reach and broad banking coverage. However, they may involve correspondent banks, intermediary deductions, and longer settlement times in certain corridors.

Where available, local payout networks can reduce both costs and settlement delays by allowing payments to be delivered through domestic banking infrastructure in the recipient's country. This approach often minimizes intermediary-bank involvement and improves cost predictability.

For recurring business payments, ACH-style transfers, domestic clearing systems, and wallet-based payouts may provide a more economical alternative, provided they meet the required settlement timelines and recipient expectations.

Businesses operating across multiple currencies can also benefit from multi-currency accounts, reducing the need for repeated currency conversions when receiving and making payments in the same currency.

Stablecoin-based settlement is emerging as another option for selected corridors, particularly where businesses need faster treasury movement or 24/7 settlement. However, these models require careful evaluation of regulatory requirements, custody arrangements, liquidity, accounting treatment, and local payout capabilities before implementation.

Also read: Fastest Cryptocurrencies for Cross-Border Payments

Rather than selecting one cross-border payment method for every transaction, businesses should define routing policies based on the characteristics of each payment segment. The most cost-effective route is the one that balances price, speed, operational reliability, and compliance for that specific payment.

If you're evaluating how modern payment providers enable different payment routes, settlement methods, and integrations, read our Cross-Border Payments API guide to understand the infrastructure behind international payment workflows.

Read in detail: Cross-Border Payment Use Cases: Practical Business Examples

For many international businesses, foreign exchange is the largest cost component of a cross-border payment. Yet it often receives less attention than transfer fees during provider evaluations.

A provider may advertise competitive transaction pricing while recovering costs through wider exchange-rate spreads. On high-value payments, even small differences in FX pricing can have a greater financial impact than the payment fee itself.

The first step is to benchmark every conversion against a reliable mid-market reference captured at the time the payment is executed. This helps finance teams understand the true spread being charged rather than relying solely on quoted rates.

Businesses with consistent payment volumes should also negotiate corridor-specific FX pricing instead of accepting standard rates across all markets. Payment volumes, currency pairs, and average transaction sizes often provide opportunities for better commercial terms.

Where operationally appropriate, multi-currency accounts can reduce unnecessary conversions by allowing businesses to hold and spend currencies they already receive. This approach works particularly well for organizations with recurring inflows and outflows in the same currency.

Treasury teams should also establish clear policies around rate locks, currency exposure, and approval thresholds. Lower FX costs should never come at the expense of unmanaged exchange-rate risk or delayed supplier payments.

Ultimately, reducing FX costs is about improving pricing discipline while maintaining predictable settlement and financial controls, not simply finding the lowest quoted exchange rate.

One of the most effective ways to lower cross-border payment costs is to reduce reliance on long correspondent banking chains wherever practical.

Instead of sending every payment as a traditional international wire, some providers settle funds locally in the destination market and complete the final leg using domestic payment infrastructure. This can reduce intermediary deductions, improve settlement predictability, and simplify the recipient experience.

Local payout capabilities are particularly valuable for businesses that regularly pay suppliers, contractors, employees, or marketplace participants in the same countries. Rather than treating every transaction as an international transfer, businesses can often benefit from domestic clearing systems or local banking networks where coverage exists.

However, local payout should not be assumed to be cheaper in every scenario. Before changing routes, businesses should evaluate:

The objective isn't simply to replace international wires, it is to determine whether a local payout model delivers lower overall cost while maintaining operational reliability.

Many businesses focus on negotiating payment fees while overlooking operational improvements that can reduce costs just as effectively.

For recurring international payments, batching multiple transfers into scheduled payment runs can reduce processing effort, simplify approvals, and improve reconciliation. Instead of sending individual payments throughout the day, finance teams can consolidate routine payouts into planned settlement windows.

Intercompany payments also benefit from netting arrangements where appropriate. Rather than moving funds between entities multiple times, offsetting receivables and payables can significantly reduce transaction volumes and associated costs.

Payment timing matters as well. Scheduling approvals before banking cut-off times and avoiding unnecessary same-day transfers helps prevent premium fees without affecting business outcomes. Not every payment requires immediate settlement, and routing policies should reflect actual urgency rather than defaulting to the fastest option.

Operational efficiency should never compromise supplier relationships or contractual payment obligations. The goal is to eliminate unnecessary costs while ensuring payments continue to arrive when expected.

Many payment delays and investigations begin long before funds leave the account. Incomplete or inaccurate beneficiary information frequently results in returned payments, compliance reviews, and manual intervention.

Common issues include incorrect bank identifiers, inconsistent beneficiary names, missing regulatory fields, incomplete addresses, or insufficient payment references. These problems not only increase operational workload but also generate avoidable repair fees and settlement delays.

Improving payment data quality starts with standardized onboarding processes. Finance teams should maintain country-specific beneficiary templates, validate payment details before first use, and capture structured payment references that simplify reconciliation later.

Regular analysis of payment failures is equally valuable. Tracking return reasons over time helps identify recurring data issues, allowing teams to address root causes instead of repeatedly resolving the same exceptions.

As payment standards continue evolving toward richer structured data, businesses that invest in cleaner payment information today will be better positioned to achieve higher straight-through processing rates and lower operational costs.

Choosing the right payment provider isn't about finding the lowest transaction fee—it's about reducing the total cost of moving money while maintaining operational reliability.

When comparing providers, evaluate each one across five core areas rather than focusing on headline pricing alone.

Don't rely solely on marketing claims or global averages. Request corridor-specific pricing, settlement performance, and service-level commitments that reflect your actual payment flows.

Before migrating critical payment volumes, run a controlled pilot using one or two high-volume corridors. Compare costs, settlement times, payment exceptions, and operational effort against your existing process before making a broader rollout decision.

Improving payment economics doesn't require replacing your entire payment infrastructure. In many cases, the biggest savings come from better visibility and incremental process improvements.

Over the next 30 days, finance teams can build a strong foundation by following a structured approach.

Week 1: Export payment data from banks, providers, ERP, treasury, and finance systems. Standardize information such as payment corridors, currencies, settlement times, transfer fees, FX rates, and payment exceptions.

Week 2: Calculate the all-in cost for each payment corridor. Identify where FX spreads, intermediary deductions, payment failures, or operational effort contribute most to total costs.

Week 3: Pilot one alternative payment route for a non-critical corridor. Compare total cost, settlement speed, beneficiary experience, reconciliation effort, and payment visibility.

Week 4: Review the results, update routing policies, strengthen beneficiary data validation, and establish monthly reporting for payment costs and settlement performance.

Track these KPIs on an ongoing basis:

Treat cross-border payment optimization as a continuous finance initiative rather than a one-time vendor negotiation.

Lowering international payment costs requires more than negotiating cheaper transfer fees. Businesses also need transparent FX pricing, reliable settlement, predictable payout infrastructure, and complete visibility across every payment corridor.

Fuze Finance helps businesses simplify cross-border payments through regulated payment infrastructure, competitive FX execution, local payout capabilities across multiple markets, and real-time payment visibility. Instead of managing multiple providers for payments, settlement, and treasury operations, businesses can streamline these workflows through a single platform.

Whether you're paying global suppliers, contractors, business partners, or marketplace participants, Fuze helps reduce operational complexity while improving cost predictability and settlement efficiency.

%20(1)%20(1).png)