Moving money internationally is far more complex than sending a payment request from one bank to another. Every transaction passes through a combination of payment rails, foreign exchange, compliance checks, settlement processes, and reconciliation workflows before funds reach the recipient.

A cross-border payments API brings these components together through a single integration. Instead of building separate connections to banks, payment networks, compliance providers, FX partners, and treasury systems, businesses can access them through one programmable interface.

The right API, however, depends on more than technical documentation. Developers need reliable integrations, finance teams need predictable costs and reporting, while operations teams need visibility into every stage of the payment lifecycle.

This guide explains how cross-border payments APIs work, why they can improve international payments, and what businesses should evaluate before selecting a provider.

A cross-border payments API is a programmable interface that enables businesses to initiate, fund, convert, track, and reconcile payments across countries and currencies.

Think of the API as the control layer, not the payment rail itself. Behind a single integration, it connects to banking partners, local payment networks, SWIFT, wallets, compliance systems, FX providers, ledgering, and settlement infrastructure.

That distinction is important. The API simplifies access to global payment infrastructure, but the quality of the experience ultimately depends on the provider's corridor coverage, routing intelligence, compliance capabilities, and operational processes.

For developers, a cross-border payments API exposes endpoints for creating quotes, initiating transfers, receiving webhooks, and handling payment statuses. For finance teams, it provides greater visibility into cross-border costs, settlement timelines, reconciliation, and reporting.

Ultimately, the goal is straightforward: move money internationally with the right balance of speed, cost, reliability, compliance, and operational visibility.

Also read: What Are Cross-Border Payments?

Traditional international payments often move through correspondent banking networks, where multiple financial institutions process a transaction before it reaches the recipient.

Each intermediary introduces potential delays, additional costs, and operational uncertainty. Payments may be affected by banking hours, compliance reviews, local clearing schedules, foreign exchange processing, intermediary deductions, and manual repair workflows.

Incomplete or inaccurate beneficiary information creates another common source of delays. Missing account details, incorrect bank identifiers, or country-specific regulatory requirements can trigger payment rejections or manual intervention.

Pricing is often just as difficult to predict. While senders usually see an upfront transfer fee, intermediary bank charges, beneficiary-bank fees, and FX markups may only become visible after the payment has been processed.

Even when payment messaging travels instantly, the actual availability of funds depends on the receiving bank and local settlement processes.

This is why businesses should evaluate more than the API itself. The more important question is:

Which parts of the payment journey does the provider actually control, automate, or make visible?

Providers that combine local payout networks, automated compliance, transparent FX pricing, and real-time payment tracking typically deliver a more predictable cross-border payment experience.

Also read: Top Cryptos with the Fastest Transactions

Although modern APIs simplify integration, the underlying payment workflow remains sophisticated. A typical international payment moves through several coordinated stages.

From a technical perspective, most cross-border payments APIs expose a standard set of resources such as payers, beneficiaries, quotes, transfers, payment rails, status updates, webhook events, ledger entries, and settlement reports. Together, these objects allow applications to create payments, monitor execution, reconcile balances, and automate post-payment workflows through a consistent API.

While APIs remove much of the integration complexity, businesses still need robust processes for exception handling, customer communication, reconciliation, and operational support.

A cross-border payments API doesn't move money on its own. Instead, it routes payments through one or more underlying payment networks, selecting the most appropriate option based on the destination, currency, amount, cost, and settlement requirements.

Different providers support different combinations of payment rails, which is why the same transfer can vary significantly in cost and delivery time across platforms.

The most common payment rails include:

SWIFT remains the global standard for international bank-to-bank messaging and supports payments to virtually every country. It offers broad reach but may involve correspondent banks, making settlement slower and fees less predictable.

Many providers connect directly to domestic clearing systems such as ACH, SEPA, Faster Payments, UPI, PIX, or other local rails. These routes often reduce costs, improve delivery speed, and eliminate unnecessary intermediaries.

Where available, real-time payment systems enable near-instant settlement between participating financial institutions. Availability depends on the destination market and the receiving bank's capabilities.

Some providers like Fuze Finance, support payments through digital wallets or stablecoin infrastructure. These routes are commonly used for faster settlement, treasury operations, or digital-asset use cases where supported by regulation.

Instead of transferring funds to a bank account, some APIs can send money directly to eligible debit or prepaid cards. This is useful when recipients need immediate access to funds without a traditional bank account.

The strongest providers don't rely on a single rail. They intelligently choose the best available route based on each payment's destination, currency, value, and service-level requirements.

Businesses often assume that an API automatically makes international payments faster. In reality, the API is only the interface, the improvements come from the infrastructure behind it.

Modern providers optimize several parts of the payment lifecycle to reduce both cost and settlement time.

Instead of routing every transaction through correspondent banking networks, many providers maintain local banking relationships across multiple countries. This allows funds to be settled domestically at the destination, reducing intermediary fees and shortening settlement cycles.

Many providers also automate operational tasks that traditionally required manual intervention, including sanctions screening, beneficiary validation, FX quoting, payment routing, and reconciliation. Fewer manual touchpoints mean fewer delays and lower operational costs.

Foreign exchange is another major area of optimization. Rather than relying on static pricing, providers can source liquidity from multiple partners and generate competitive quotes based on the payment corridor and transaction size.

Real-time payment tracking also improves operational efficiency. Developers receive webhook notifications as payments progress, while finance teams gain better visibility into settlement status, failed transfers, and reconciliation.

However, faster doesn't always mean instant. Delivery times still depend on corridor availability, local banking infrastructure, regulatory checks, funding methods, and the recipient's financial institution.

When evaluating providers, focus less on marketing claims such as "instant international payments" and more on measurable operational capabilities, including corridor coverage, average settlement times, FX transparency, payment success rates, and exception handling.

Not all cross-border payments APIs solve the same problem. Some focus on developer experience, while others prioritize treasury management, local payout coverage, compliance automation, or FX optimization.

Rather than comparing feature lists, evaluate providers based on the capabilities that will affect your product after launch.

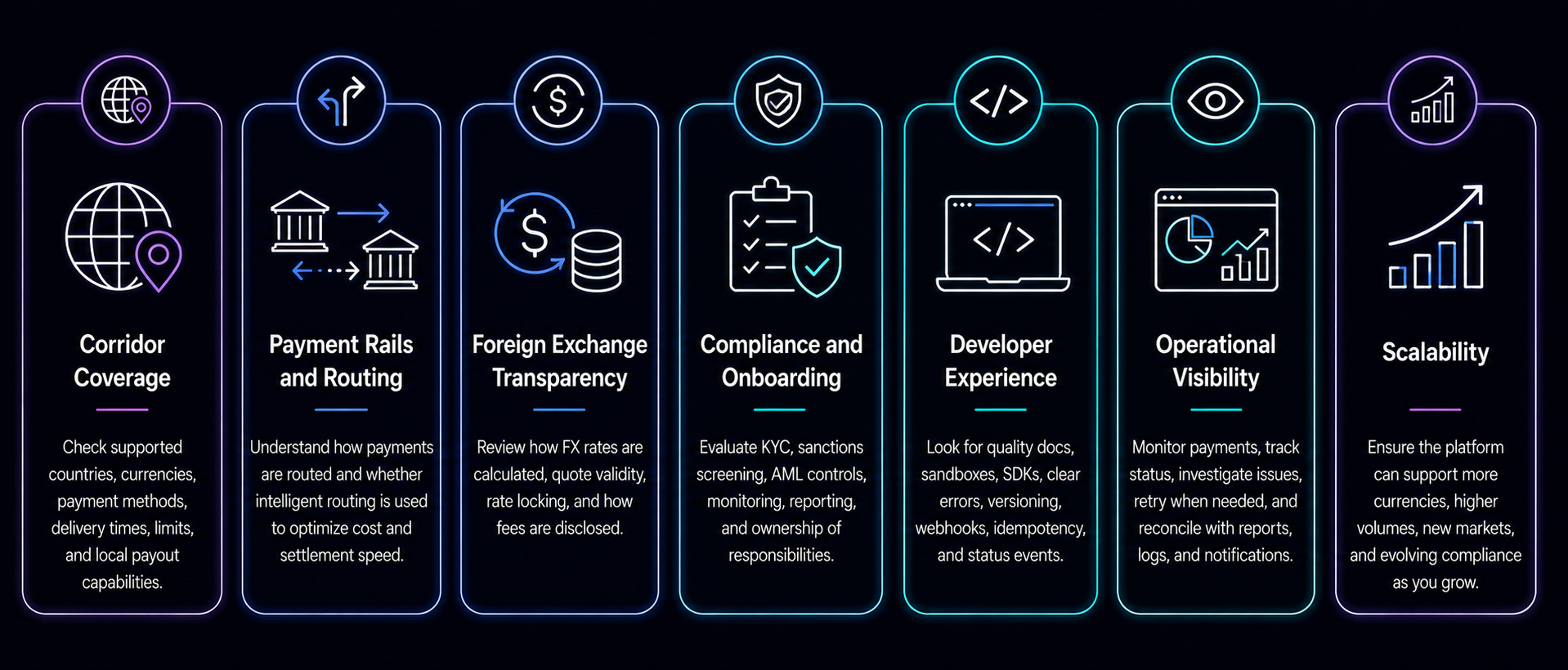

Start with the payment corridors you actually support today, and those you expect to expand into over the next few years.

A provider with excellent global coverage may still have limited payout options in your most important markets. Verify supported countries, currencies, payment methods, delivery times, transaction limits, and local payout capabilities before making a decision.

Ask how payments are routed behind the scenes.

Does the provider rely primarily on SWIFT, or can it access local clearing systems? Does it automatically choose the most efficient route based on cost and settlement speed? Intelligent routing often has a greater impact on performance than the API itself.

FX pricing is frequently the largest hidden cost in international payments.

Understand how exchange rates are calculated, how long quotes remain valid, whether rates are locked before execution, and how fees are presented. Transparent pricing makes reconciliation easier and reduces unexpected costs.

Cross-border payments are heavily regulated, making compliance one of the most important parts of the integration.

Evaluate how the provider handles identity verification, sanctions screening, AML controls, transaction monitoring, and regulatory reporting. Also clarify which responsibilities remain with your business and which are managed by the provider.

A strong API should reduce engineering effort rather than create additional operational work.

Look for comprehensive documentation, realistic sandbox environments, SDKs, clear error messages, versioning policies, idempotent requests, webhook support, and well-defined payment status events.

International payments don't always succeed on the first attempt.

Your operations team should be able to monitor payment status, investigate failures, retry transactions where appropriate, and reconcile settlements without relying on manual support requests.

Reporting dashboards, audit logs, downloadable reports, and webhook notifications become increasingly valuable as payment volumes grow.

The provider you choose should support where your business is heading, not just where it is today.

Consider whether it can support additional currencies, higher transaction volumes, new payout methods, new markets, and evolving compliance requirements without requiring another migration.

Before committing to a provider, ask practical questions that reveal how the platform performs in production, not just in product demos.

The answers to these questions often reveal more about a provider's operational maturity than a long list of API endpoints.

Choosing a cross-border payments API is not just a technical decision. Every international payment involves regulatory obligations, customer verification, sanctions screening, and reporting requirements that vary by jurisdiction.

Before selecting a provider, understand which responsibilities are handled by the platform and which remain with your business. Key areas to evaluate include:

Some providers operate under their own regulated entities and assume a larger share of compliance responsibilities, while others simply provide technology and expect customers to manage licensing and regulatory obligations themselves.

Understanding this operating model early helps avoid compliance gaps as payment volumes grow.

Not every business needs the same infrastructure. Some organizations benefit from building direct banking relationships, while others can launch significantly faster through an API provider.

Common approaches include:

Direct bank integrations provide maximum control but require substantial investment in treasury operations, compliance, maintenance, and country-specific integrations.

Cross-border payments APIs offer faster deployment by combining payment routing, FX, compliance workflows, and reporting behind a single integration.

Payment orchestration platforms can improve redundancy and routing flexibility but often introduce additional operational complexity.

Stablecoin-based infrastructure may provide advantages for treasury operations, high-friction corridors, and 24/7 settlement where regulations permit.

When comparing providers, evaluate:

The right choice depends less on brand recognition and more on how well the provider fits your product, geography, and operational model.

Before launching with any cross-border payments API, validate the entire payment lifecycle, not just whether an API call succeeds.

A controlled rollout helps identify operational issues early and reduces payment failures, support requests, and reconciliation problems as volumes grow.

Fuze Finance is designed for businesses that need to move money across borders efficiently using stablecoin infrastructure. Rather than offering a retail payment app, it provides APIs that enable fintechs, payment providers, remittance companies, marketplaces, and enterprises to embed cross-border payments directly into their products.

The platform combines stablecoin-based settlement with multi-currency accounts, wallet infrastructure, FX conversion, compliance workflows, and API-first payment orchestration. This enables businesses to send and receive international payments through a single integration while reducing operational complexity.

Fuze is particularly well suited for companies operating across the Middle East and other supported markets that require programmable payment infrastructure for treasury operations, supplier payments, remittances, payroll, or embedded financial products.

Before integrating any provider, businesses should evaluate supported corridors, settlement timelines, regulatory coverage, available currencies, pricing, and reporting capabilities to ensure the platform aligns with their operational requirements.

%20(1)%20(1).png)