Fintech teams evaluating embedded investing often start by comparing providers, APIs, and technical capabilities. In reality, the more important decision comes much earlier: understanding what kind of investment experience they want to build.

Embedded trading, embedded investing, and brokerage APIs are closely related, but they solve different customer problems. Choosing the wrong model can affect everything from product design and compliance to customer onboarding and long-term scalability.

This guide explains how the three approaches differ, when each one makes sense, and how to choose the right model before evaluating infrastructure providers.

Many fintech products rely on similar building blocks, customer accounts, funding, portfolios, order execution, and reporting. Because of that, embedded trading, embedded investing, and brokerage APIs can appear to solve the same problem.

The real difference lies in the customer experience you're trying to create.

If users open your app because they want to execute trades, you're building an embedded trading experience. If the goal is to help customers invest consistently toward long-term financial goals, you're building embedded investing. If your engineering team simply needs regulated infrastructure to power either experience, you're evaluating brokerage APIs.

That decision influences almost everything that follows, from onboarding and compliance to custody, product design, customer support, and partner selection.

A simple way to think about it is:

The technology powering these models can look similar, but the customer journey, business objectives, and operating model are often very different.

Before comparing providers or evaluating APIs, it's helpful to understand how these three concepts relate to one another.

Embedded trading allows users to buy and sell financial assets directly within an existing application instead of leaving for a separate brokerage platform. Trading becomes another feature inside a banking app, fintech product, wealth platform, or payroll application.

The emphasis is on execution. Users decide what they want to buy or sell, and the platform provides the trading experience while regulated infrastructure handles functions such as execution, custody, and settlement.

Read in detail: What Is Embedded Trading?

Embedded investing is a broader category focused on helping users build wealth over time. While trading may be part of the experience, investing products often emphasise recurring contributions, diversified portfolios, retirement planning, or automated investment strategies rather than frequent buying and selling.

Many products position investing as a natural extension of existing financial behaviours, such as saving, receiving income, or managing long-term financial goals.

Brokerage APIs sit behind both embedded trading and embedded investing experiences. They provide the regulated infrastructure that allows applications to create investment accounts, verify customers, route orders, manage portfolios, and support post-trade operations.

Unlike embedded trading or investing, brokerage APIs are not customer-facing products. They are the technology layer developers integrate to build investment experiences.

Although these terms are closely related, they describe different layers of a financial product.

Embedded trading and embedded investing define the customer experience, while brokerage APIs provide the infrastructure that powers those experiences behind the scenes. Understanding where each model fits makes it much easier to evaluate providers, estimate implementation effort, and design the right product.

The table below highlights the key differences.

Embedded trading is designed for products where users want to make their own investment decisions and execute trades without leaving the platform. Instead of redirecting customers to a separate brokerage, trading becomes part of the existing product experience.

This model works best when investing is already a natural extension of how customers use the product. For example, a neobank may allow users to invest idle cash, while a wealth platform might let customers act on portfolio recommendations immediately.

Common embedded trading use cases include:

The focus is on giving customers direct control over their investments while keeping the experience within a familiar application.

Many fintechs choose embedded trading because it improves customer engagement without requiring users to manage multiple financial apps. Behind the scenes, regulated embedded trading infrastructure providers typically support functions such as account opening, order execution, custody, and settlement.

Not every customer wants to trade. Many simply want an easier way to invest regularly and build long-term wealth.

Embedded investing focuses on helping users achieve financial goals through recurring contributions, diversified portfolios, retirement planning, or automated investment strategies. Instead of encouraging frequent trading, these products emphasise consistency, education, and long-term outcomes.

Typical examples include:

For many fintech products, this approach feels more natural than a traditional trading interface. A payroll platform, for example, is better suited to salary-linked investing than active stock trading, while a budgeting app may encourage customers to invest surplus savings automatically.

The objective isn't simply to provide market access, it's to make investing easier at the moment customers are already making financial decisions.

Once a product team has decided what investment experience it wants to build, the next step is selecting the infrastructure that will support it.

Brokerage APIs provide the technology layer behind embedded trading and embedded investing. Rather than interacting with end users, they allow developers to integrate regulated investment functionality into their own applications.

Depending on the provider, brokerage APIs may support:

The exact capabilities vary significantly between providers. Some focus on self-directed investing, while others specialise in wealth management, retirement products, or digital assets. Geographic coverage, licensing, supported asset classes, and operational responsibilities also differ.

For this reason, fintech teams should evaluate brokerage APIs based on how well they support the product they want to build, not simply on the number of available endpoints.

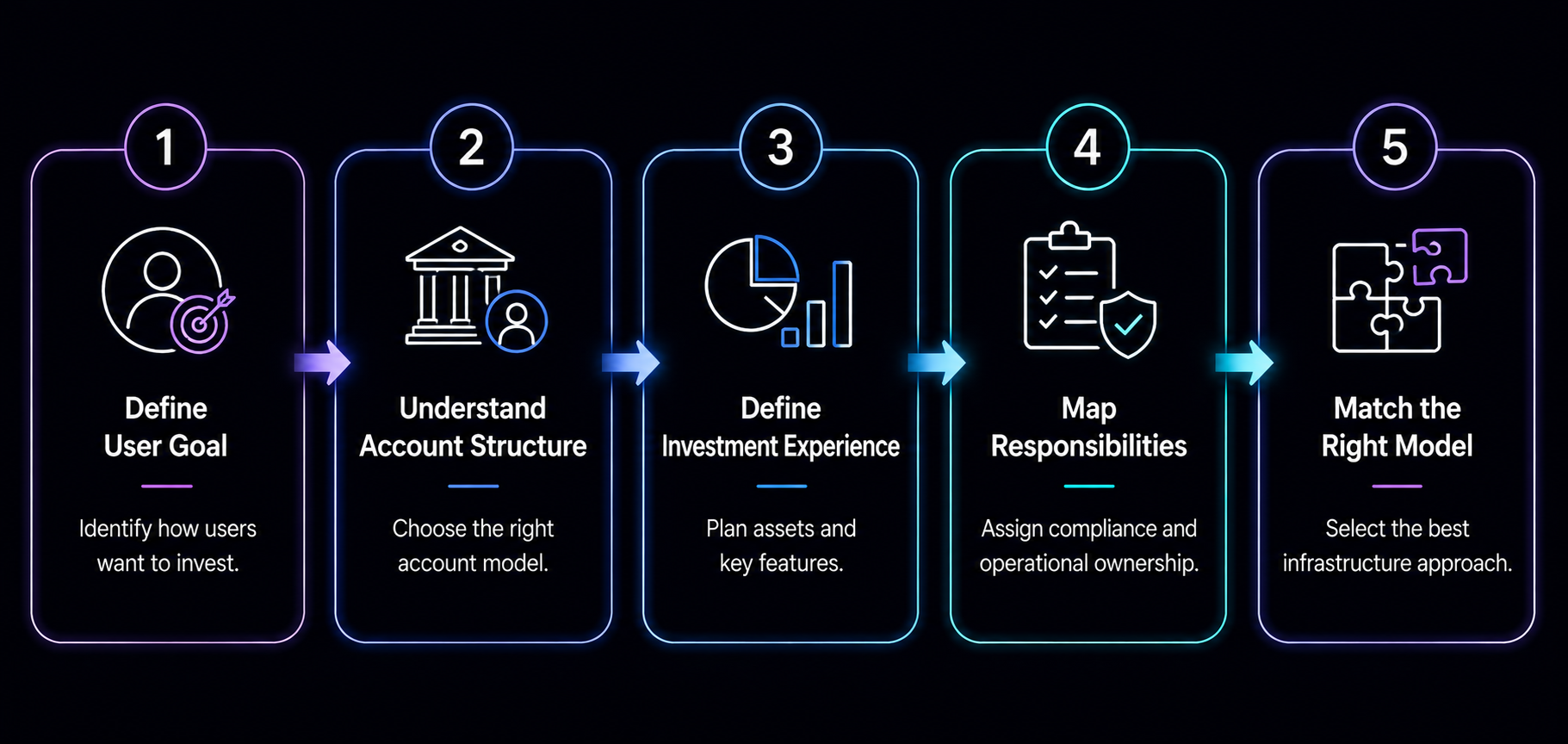

Before comparing providers or reviewing API documentation, step back and define the investment experience you want to create. The right infrastructure becomes much easier to identify once you're clear about what users are trying to accomplish.

Work through the following questions before evaluating any embedded investing or brokerage platform.

Start by understanding the action the customer wants to take.

Ask yourself:

The answer helps determine whether you're building a trading experience, an investing product, or simply connecting to existing brokerage accounts.

Next, consider how investment accounts will be created and managed.

Questions to answer include:

Account structure influences onboarding, compliance, reporting, and operational responsibilities.

Think beyond the first release and consider the long-term product roadmap.

For example:

Launching an investment product involves more than customer-facing features.

Clearly identify which organisation is responsible for:

A documented responsibility matrix reduces implementation risk and avoids confusion after launch.

Once these decisions are clear, selecting the right model becomes much simpler.

The most successful fintech products choose infrastructure that supports the customer experience, not the other way around.

Another important consideration is how much influence your product has over investment decisions. An execution-only experience differs from one that recommends investments or manages portfolios, and that distinction can affect both product design and regulatory obligations.

Adding an investment feature isn't simply an API integration. Behind every trading screen sits a broader operating model that supports customer onboarding, compliance, funding, execution, reporting, and ongoing support.

Exactly what you need depends on the product you're building, but most embedded investment experiences require capabilities across the following areas.

The scope varies considerably between products. A lightweight trading feature may require little more than order execution and portfolio data, while a full investment platform needs durable operational processes that support customers throughout the account lifecycle.

The same underlying infrastructure can support very different financial products. What changes is the customer promise, operating model, and regulatory responsibilities.

Here are a few common examples.

A digital bank introducing fractional stock investing will typically need embedded investing infrastructure, including onboarding, funding, portfolio management, recurring investments, statements, and customer support.

A portfolio management app that introduces buy and sell functionality may require embedded trading or brokerage connectivity, depending on whether customers trade through existing brokerage accounts or new accounts created within the platform.

Products centred on automated investing usually combine advisory capabilities with brokerage infrastructure to support portfolio recommendations, recurring investments, and automated rebalancing.

Developer tools generally prioritise brokerage APIs and trading infrastructure rather than consumer-facing investment experiences. The primary users are developers building financial products rather than retail investors.

When the objective is helping customers build wealth over time, embedded investing is often the best fit because it aligns with recurring contributions, diversified portfolios, and long-term financial planning.

Products offering crypto investing or fiat-to-crypto conversion typically require embedded trading infrastructure with support for digital asset onboarding, execution, custody, and settlement.

Also read: Embedded Trading Use Cases for Fintech Product Teams

Provider terminology varies widely. Rather than relying on marketing labels such as embedded investing or brokerage-as-a-service, evaluate providers against the capabilities your product actually requires.

Key evaluation areas include:

During due diligence, verify exactly what the provider delivers. An "embedded investing platform" may include a completely regulated operating model, or it may simply provide APIs or a front-end widget. Understanding where responsibilities begin and end is just as important as comparing technical features.

Fuze Finance provides API-first embedded trading infrastructure designed for fintechs, banks, payment providers, and wealth platforms that want to integrate investment capabilities without building regulated trading infrastructure from scratch.

Its platform supports digital asset trading through developer-friendly APIs, institutional liquidity, custody integrations, onboarding workflows, and operational infrastructure that can help businesses launch embedded investment products more efficiently.

Like any infrastructure provider, Fuze should be evaluated against your product requirements, target markets, regulatory obligations, and long-term roadmap. Businesses should review documentation, supported jurisdictions, operational capabilities, and commercial terms as part of their due diligence before selecting a partner.

%20(1)%20(1).png)