Embedded trading is no longer just for investment apps. Today, neobanks, payroll providers, wealth platforms, and vertical SaaS companies are exploring how to let customers invest without leaving the products they already use.

But adding trading isn't simply about integrating a brokerage API. The strongest products introduce investing at moments where customers are already making financial decisions, whether they're receiving a paycheck, building savings, managing business cash flow, or planning for retirement.

This guide explores the most practical embedded trading use cases for fintech product teams, explains where the model delivers the most value, and outlines what businesses should evaluate before bringing investing into their platform.

Before comparing providers or evaluating APIs, product teams should answer a more fundamental question: does investing naturally fit into the customer journey?

Embedded trading works best when users are already managing money within the product. They might be receiving income, holding balances, saving toward a goal, reviewing investments, or planning for retirement. In these moments, offering investing feels like a natural extension of the experience rather than a separate product.

Some common examples include:

Adding trading changes much more than the user interface. It introduces new considerations around compliance, customer support, operational workflows, risk management, and revenue models.

The strongest product teams don't begin with technology, they begin by identifying the financial action users already want to take and then determine whether investing is the right next step.

Embedded trading allows users to buy, sell, or manage investments inside an application that isn't primarily a brokerage. Depending on the product, this may include stock trading, ETF investing, watchlists, portfolio tracking, or recurring investments.

It's useful to distinguish three closely related concepts:

Different embedded trading providers support investing in different ways. They vary significantly in licensing, supported assets, geographic coverage, and operating models, so the right choice depends on the needs of the product rather than a simple feature comparison.

For customers, investing appears as another feature inside the app. Behind the scenes, however, the business is delivering a regulated financial product that requires appropriate operational and compliance support.

Not every fintech product benefits from embedded trading. Before investing in infrastructure, it's worth evaluating whether investing naturally fits the way customers already use your platform.

Products are generally stronger candidates when users already hold balances, receive income, save money, or return frequently enough for investing to become part of an ongoing financial relationship. Customers should also trust the product with important financial decisions and have a clear reason to invest, whether that's growing idle cash, saving for long-term goals, or planning for retirement.

By contrast, embedded trading is usually a weaker fit for products that are purely transactional or where users rarely hold funds inside the platform. In those cases, payments, savings, lending, or insurance may solve more immediate customer needs.

A useful test is to ask one simple question:

What investment action would users naturally want to take at this exact moment?

If there isn't a clear answer, the product may need stronger financial engagement before investing becomes a meaningful addition.

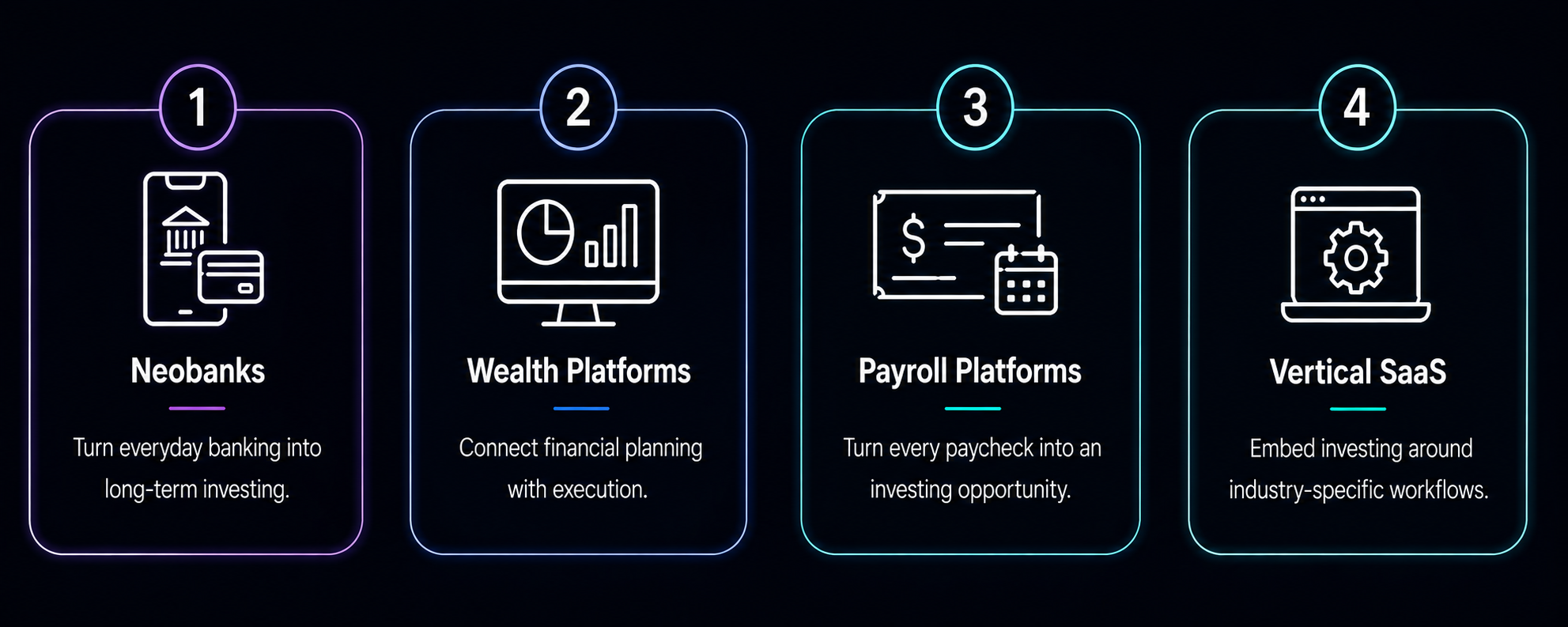

Embedded trading isn't a single product. The way it's implemented depends on the financial role your platform already plays in a customer's life.

For some businesses, investing is a natural extension of everyday banking. For others, it's a way to connect financial planning with execution or turn recurring income into long-term wealth. The following examples illustrate where embedded trading creates the most value today and why the right starting point differs across product categories.

Neobanks are one of the strongest candidates for embedded trading because customers already manage their day-to-day finances within the app. They receive salaries, pay bills, transfer money, save towards goals, and monitor their balances, creating natural opportunities to introduce investing without disrupting the experience.

Rather than asking customers to open a separate brokerage account, investing becomes another step in an existing money journey. A customer who has built an emergency fund, for example, can be encouraged to start investing a small recurring amount instead of leaving excess cash idle.

Common approaches include:

DriveWealth has reported that more than 15 million customers accessed fractional U.S. equity investing through its global partner network, demonstrating how embedded investing has already become part of the modern neobank experience. This figure reflects historical platform data and should be interpreted as an example of market adoption rather than a measure of current activity.

Product insight: For most neobanks, the first embedded investing feature should reinforce existing saving habits rather than encourage frequent trading.

Many wealth platforms already help users understand their finances through budgeting tools, retirement projections, portfolio analytics, or financial planning. Embedded trading allows those insights to become actionable by enabling users to invest without leaving the platform.

The right starting point depends on the product's existing value proposition. A planning tool may introduce model portfolios or recurring investments, while a portfolio tracker may focus on trade execution and rebalancing. Advisor platforms often prioritise client portals and managed investment workflows rather than self-directed trading.

Typical capabilities include:

Platforms such as Apex Fintech Solutions provide infrastructure for many of these capabilities, including rebalancing, model portfolios, direct indexing, and advisor workstations. The appropriate implementation, however, depends on whether the platform primarily serves self-directed investors, financial advisers, or managed investment products.

Fuze Finance also supports this category by providing embedded trading infrastructure that enables fintechs and wealth platforms to integrate investing without building regulated trading operations internally.

Product insight: Wealth products should begin with the investment experience that best matches existing customer intent. Users seeking guidance often respond better to portfolios and recurring investing than unrestricted trading.

Payroll platforms create one of the most predictable investing moments in financial services: payday.

Unlike trading apps, payroll products are centred on recurring income rather than market activity. That makes them particularly well suited to long-term investing, where contributions happen automatically as part of each pay cycle.

Instead of encouraging active trading, payroll platforms typically focus on helping employees build wealth gradually through recurring contributions and retirement planning.

Common examples include:

Solutions such as Paylocity Retirement, powered by Vestwell, integrate retirement contributions directly into payroll workflows, while Human Interest enables payroll providers and financial institutions to embed or white-label retirement products within their own platforms.

These examples illustrate that payroll investing is fundamentally different from brokerage-style trading. The objective is to help users invest consistently from earned income rather than react to market movements.

Product insight: For payroll platforms, recurring investing and retirement products are usually a stronger first step than self-directed stock trading.

Vertical SaaS platforms present a different opportunity. While they often manage payments, invoices, contractor earnings, or business cash flow, investing is rarely the first embedded finance product they should introduce.

The strongest opportunities emerge when the platform already controls meaningful financial events or holds customer balances for extended periods. In those situations, investing can become a logical extension of the workflow.

Potential examples include:

However, many vertical SaaS businesses should prioritise payments, lending, treasury, or insurance before introducing investing. Unless customers already have investable balances or clear investment intent, trading may feel disconnected from the product's core value.

Product insight: Rather than asking whether trading can be embedded, ask whether investing naturally follows the financial workflow your customers already complete inside the platform.

Embedded trading can strengthen a fintech product in several ways, but the benefits depend on how well the investment experience fits the existing customer journey. Simply adding trading features is unlikely to improve engagement unless users already have a reason to invest within the platform.

When implemented thoughtfully, embedded trading can increase customer engagement by giving users more reasons to return. Instead of opening the app only to check a balance or make a payment, users may come back to review portfolios, monitor recurring investments, rebalance holdings, or access educational content.

It can also improve retention. As customers build investment balances over time, the platform often becomes a larger part of their financial life, making it less likely they'll switch to another provider.

For many businesses, embedded trading also creates opportunities to diversify revenue through partner revenue sharing, advisory fees, subscription models, or other permitted commercial arrangements. The exact model depends on licensing, product design, and regulatory requirements.

Perhaps the biggest advantage is the opportunity to deepen customer relationships. A product that starts with payments or banking can gradually expand into savings, investing, and wealth management, increasing customer lifetime value without requiring users to adopt multiple financial apps.

The benefits, however, come with new operational responsibilities. Supporting investing means handling trade-related support requests, funding issues, tax documents, fraud monitoring, regulatory communications, and customer education.

Product insight: Embedded trading should be viewed as a long-term product expansion rather than a feature designed to increase short-term engagement.

Once a product team has identified a clear use case, the next step is understanding everything required to support an investing experience. While modern infrastructure providers simplify much of the technical implementation, launching embedded trading involves far more than integrating an API.

A typical launch journey includes:

Infrastructure providers such as Fuze Finance can reduce much of the engineering effort by providing embedded trading APIs and regulated infrastructure. Even so, product teams remain responsible for the customer experience, educational content, lifecycle messaging, support processes, and ongoing operational oversight.

Product insight: A successful MVP focuses on solving one customer problem well rather than launching every investing feature on day one.

Good product design is just as important as technical implementation. The way investing is presented can influence customer behaviour, making user experience an important part of responsible product development.

Product teams should prioritise clear communication over engagement mechanics that encourage unnecessary trading. Educational content, transparent pricing, realistic risk disclosures, and straightforward onboarding generally create stronger long-term outcomes than features designed to increase trading frequency.

Important considerations include:

Regulators continue to examine how digital interfaces influence investor behaviour, particularly where gamification or behavioural prompts could encourage unsuitable trading activity. Building a simple, transparent investing experience is therefore not only good product design but also good risk management.

Product insight: The safest first product is usually the simplest one, focused on long-term investing rather than frequent trading.

The best embedded trading strategy depends on the financial role your product already plays in customers' lives. Rather than launching a broad investing platform, many successful fintechs begin with a single use case that aligns closely with existing user behaviour.

A practical rollout often follows a simple sequence:

Embedded trading delivers the greatest value when it simplifies an existing financial decision rather than introducing a completely new behaviour.

Adding investing to a fintech product requires more than market access. Businesses also need regulated infrastructure, reliable liquidity, onboarding workflows, custody, reporting, and developer tools that can support long-term growth.

Fuze provides API-first embedded trading infrastructure that enables fintechs, banks, payment providers, and wealth platforms to integrate digital asset trading into their existing products. The platform combines institutional liquidity, regulated onboarding, custody integrations, and developer-friendly APIs, helping businesses launch embedded trading without building brokerage infrastructure from scratch.

Whether you're exploring embedded trading for the first time or expanding an existing financial product, Fuze provides the infrastructure to support a faster launch while allowing product teams to focus on delivering a seamless customer experience.

%20(1)%20(1).png)