Crypto OTC trading has moved from a niche execution channel to a major institutional market-structure layer. Instead of relying only on public exchange order books, funds, market makers, payment companies, treasuries, and high-net-worth traders increasingly use private execution workflows for large trades, settlement flexibility, and reduced market impact.

This brief explains the latest 2025–Q1 2026 statistics, why OTC volume is difficult to measure, and what the numbers suggest about institutional adoption, stablecoin settlement, and execution quality. The key theme is clear: crypto OTC is not a fully transparent exchange-style market, but reported platform and desk data offer useful signals about where institutional digital asset trading is heading.

The following figures should be read as directional indicators from platform and desk samples, not a complete census of the private OTC market. Crypto OTC activity is private, fragmented, and usually measured through proprietary platform data, desk-reported data, or institutional surveys.

Key statistics from recent reported samples include:

The strongest interpretation is not that the entire OTC market is a single, precisely measurable dollar amount. Rather, available samples show a market becoming more institutional, more stablecoin-dependent, and more execution-quality focused.

Crypto OTC (over-the-counter) trading is the private buying and selling of digital assets outside a public exchange order book. Instead of placing an order on an exchange where everyone can see it, buyers and sellers negotiate the trade directly through an OTC desk or broker.

A typical OTC trade starts when a client requests a quote for a specific cryptocurrency and trade size. The OTC desk then provides a price, and once both parties agree, the trade is settled privately. This allows large transactions to take place without affecting prices on public exchanges.

Businesses and institutional investors often prefer OTC trading because it offers several practical advantages. Large trades can usually be executed with less market impact, reducing the chance of moving prices while the order is being filled. It can also help minimize slippage, keep trading activity private, and provide more flexible settlement options using fiat currencies, stablecoins, or cryptocurrencies.

In simple terms, crypto OTC trading is designed for businesses and investors that need to execute large trades securely, privately, and efficiently.

Read in detail: What is a Crypto OTC Desk?

Unlike centralized exchanges, the crypto OTC market has no single public order book or reporting system. Most trades take place privately between institutions, brokers, market makers, and liquidity providers, making it difficult to measure the market's total size accurately.

As a result, most OTC statistics come from proprietary platform data, individual trading desks, or institutional surveys. Each source provides a different perspective. Platform data can reveal trading trends within a particular network, desk-reported data highlights client activity and execution patterns, while institutional surveys offer insight into adoption and market sentiment. Public exchange data, on the other hand, only reflects trading that occurs on exchanges and doesn't capture private OTC transactions.

For this reason, it's best to treat OTC market statistics as indicators of broader market trends rather than exact measurements of the industry's total size. Looking at multiple credible sources over time provides a much clearer picture than relying on a single figure or estimate.

The recent growth arc is best understood as a timeline.

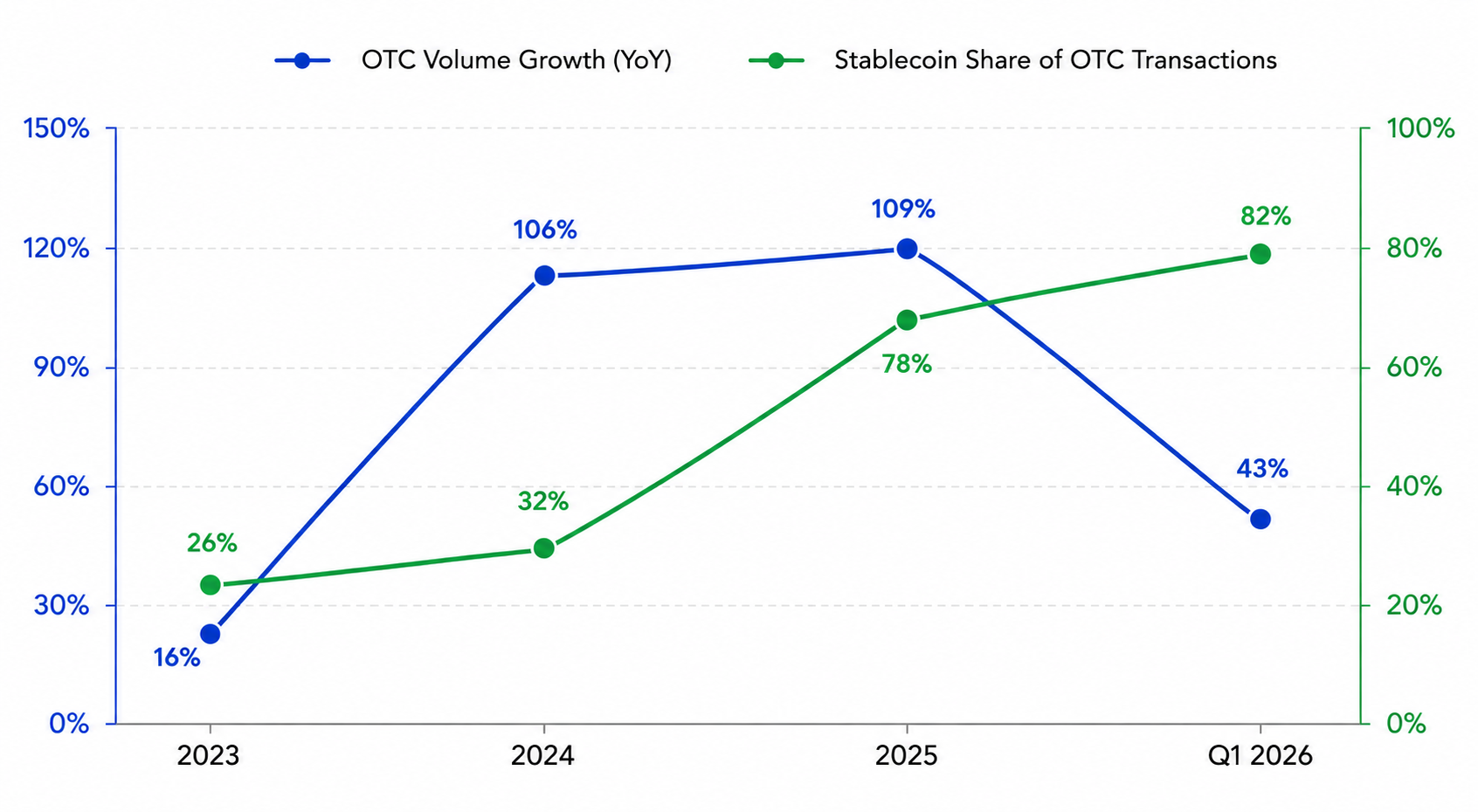

1. 2024: Finery reported crypto OTC trading volume up 106% YoY, describing the year as record-breaking for institutional and large-scale digital asset transactions.

2. 2025: Finery reported crypto spot OTC markets up 109% YoY, exceeding the 10%–60% growth expectations it said stakeholders had forecast at the start of the year. Transaction count also rose 100% YoY, showing the expansion was not only driven by a small number of larger trades.

3. Q1 2026: OTC spot volume rose 43% YoY. That is still positive growth, but it is much lower than the elevated 2024–2025 baseline.

The shift looks more like maturation and normalization than a collapse. After a major expansion cycle, institutional flows appear to have become more selective, more risk-aware, and more execution-focused. Growth compressed, but it remained positive.

OTC demand is not just “big whale trades.” It reflects a broader institutional need for controlled execution, settlement reliability, governance, and counterparty management.

Common OTC users include:

Broader survey data supports this institutionalization. EY-Parthenon and Coinbase surveyed more than 350 institutional investors globally in January 2026, including asset managers, asset owners, family offices, private banks, hedge funds, and VC firms. In that survey, 73% of respondents planned to increase digital asset allocations in 2026.

Importantly, the same survey emphasized that institutions are pairing allocation intent with more disciplined risk, liquidity, position-sizing, and governance practices.

Crypto market structure is becoming more multi-venue. CEXs, DEXs, and OTC desks each solve different execution problems.

In Q1 2026, Finery reported OTC volume up 43% YoY. Over the same period, it reported top-20 DEX volume up 39% YoY and top-20 CEX volume down 45% YoY. Finery described this as a continuation of venue rebalancing observed in 2025.

This does not mean centralized exchanges are obsolete. It suggests institutional trading is becoming more multi-venue, with OTC rails gaining relative importance for large-block execution where discretion, reduced market impact, and capital efficiency matter.

Also read: OTC Desk Vs Exchange

BTC remains central to institutional OTC activity, but ETH gained share sharply in Q1 2026 in Finery’s sample.

In Q1 2026, ETH and BTC together represented 74% of institutional OTC volume, up from 62% in Q1 2025. ETH’s share rose from 20% to 41% year over year, while BTC’s share moved from 42% to 33%.

Finery cautioned that ETH’s expansion is still early to interpret conclusively. Possible drivers include Ethereum layer-2 infrastructure, tokenization use cases, and ETF-related flows. Overall, the quarter looked more like a reweighting within major assets than broad-based expansion across the full token spectrum.

The reader takeaway is straightforward: institutional OTC liquidity is concentrated around majors, not spreading evenly across all crypto assets.

Also read: Best USDT Networks

Stablecoins are no longer just trading pairs. They are becoming settlement infrastructure.

In 2025, stablecoins represented 78% of all OTC transactions processed through Finery’s liquidity network, up from 26% in 2023. Finery also reported 119% YoY stablecoin volume growth in 2025.

The trend continued into 2026. In Q1 2026, Finery reported stablecoin OTC volumes up 59% YoY. It also reported that crypto-to-stablecoin flows rose 82% YoY, while crypto-to-fiat and crypto-to-crypto conversions contracted. Stablecoins accounted for 82% of total trades in Finery’s Q1 2026 sample, up from 76% in Q1 2025.

The operational reason is clear: stablecoins help OTC desks and institutions settle in a dollar-linked or fiat-linked unit without always returning to traditional bank rails. They can support 24/7 settlement and faster movement of value.

However, stablecoins also introduce risks, including reserve quality, depeg events, issuer exposure, chain risk, redemption constraints, and jurisdictional uncertainty. Coinbase and EY’s 2026 survey also found that stablecoins have moved beyond trading facilitation, with institutions using or considering them for cash management, money movement, and near-real-time settlement.

Stablecoin share is therefore one of the most important OTC indicators to watch because it connects trading liquidity, settlement speed, and institutional operating models.

Modern crypto OTC execution is more than a trader calling a desk for a quote. Institutions now use a range of workflows:

Wintermute reported that its OTC options activity more than doubled YoY in 2025, with year-end notional volumes almost four times higher than at the start of the year and trade counts more than twice as high.

Because this is proprietary, desk-specific data, it should not be treated as a universal market total. Still, it suggests OTC is becoming not only a spot access channel, but also a risk-transfer and portfolio-construction layer.

The practical problem OTC solves is execution quality at size. Large public orders can consume multiple levels of an order book, creating slippage between expected and actual execution price. They can also reveal trading intent, invite adverse price movement, or create market impact before the full order is complete.

For institutions, OTC evaluation is therefore not only about headline price. It includes total execution cost, certainty, settlement speed, counterparty quality, and operational risk.

The table below is illustrative and hypothetical, not market data.

A simple calculation shows why this matters. If a $25 million order suffers 30 bps of all-in execution cost, the cost is $75,000. If improved OTC execution reduces cost by 10 bps, the savings are $25,000.

That is why institutions often care as much about process, liquidity sourcing, and settlement reliability as they do about the first quoted price.

OTC trading offers benefits, but institutional users need a rigorous risk checklist.

Key risks include:

Coinbase and EY-Parthenon reported that 49% of surveyed institutions strengthened their emphasis on risk management, liquidity, and position sizing. The same survey summary reported that 66% cited regulatory compliance as a key custodian-selection factor in 2026, up from 25% in 2025, and 66% cited security/key-signing protocols, up from 8% in 2025.

EY’s version of the survey also noted that risk, regulation, and custody security have moved from “considerations” to “decision drivers.”

The practical takeaway: OTC desk selection should include pricing quality, liquidity access, settlement process, counterparty controls, custody compatibility, compliance support, and operational resilience.

Choosing the right crypto OTC desk goes beyond pricing or liquidity. Businesses also need a partner that offers secure settlement, regulatory compliance, reliable execution, and the operational support to manage large digital asset transactions with confidence.

Fuze Finance provides a regulated, enterprise-grade OTC trading solution designed for banks, fintechs, payment providers, exchanges, and enterprises. Clients can buy and sell a wide range of cryptocurrencies and stablecoins with competitive pricing, deep liquidity, flexible settlement options, and dedicated support.

Beyond OTC trading, Fuze offers a complete digital asset infrastructure platform, including stablecoin payments, embedded wallets, treasury management, and custody solutions. This enables businesses to manage trading, settlements, and digital asset operations through a single regulated provider instead of coordinating multiple vendors.

Whether you're executing large block trades, managing corporate treasury, or building crypto products for your customers, Fuze helps you trade digital assets securely, efficiently, and at scale.

Explore Fuze OTC Trading