The difference between OTC and exchange in crypto is a matter of scale. Both methods let you trade crypto, but once trade sizes reach institutional levels, the mechanics diverge sharply. That divergence determines whether you get the price you expected, whether your order moves the market against you, and whether your bank accepts the settlement proceeds.

OTC trading is not a crypto invention. It has been the standard execution model in traditional finance for equities, foreign exchange, and bonds for decades, and crypto adopted it for the same reason: public order books were not built to absorb institutional volume efficiently.

According to Finery Markets' 2026 institutional OTC trading report, institutional spot OTC volumes expanded 109% year over year, while the top-20 centralized exchanges grew just 9% over the same period. For anyone evaluating crypto OTC vs. exchange trading at an institutional scale, that gap reflects a structural shift in how professional capital moves through crypto markets.

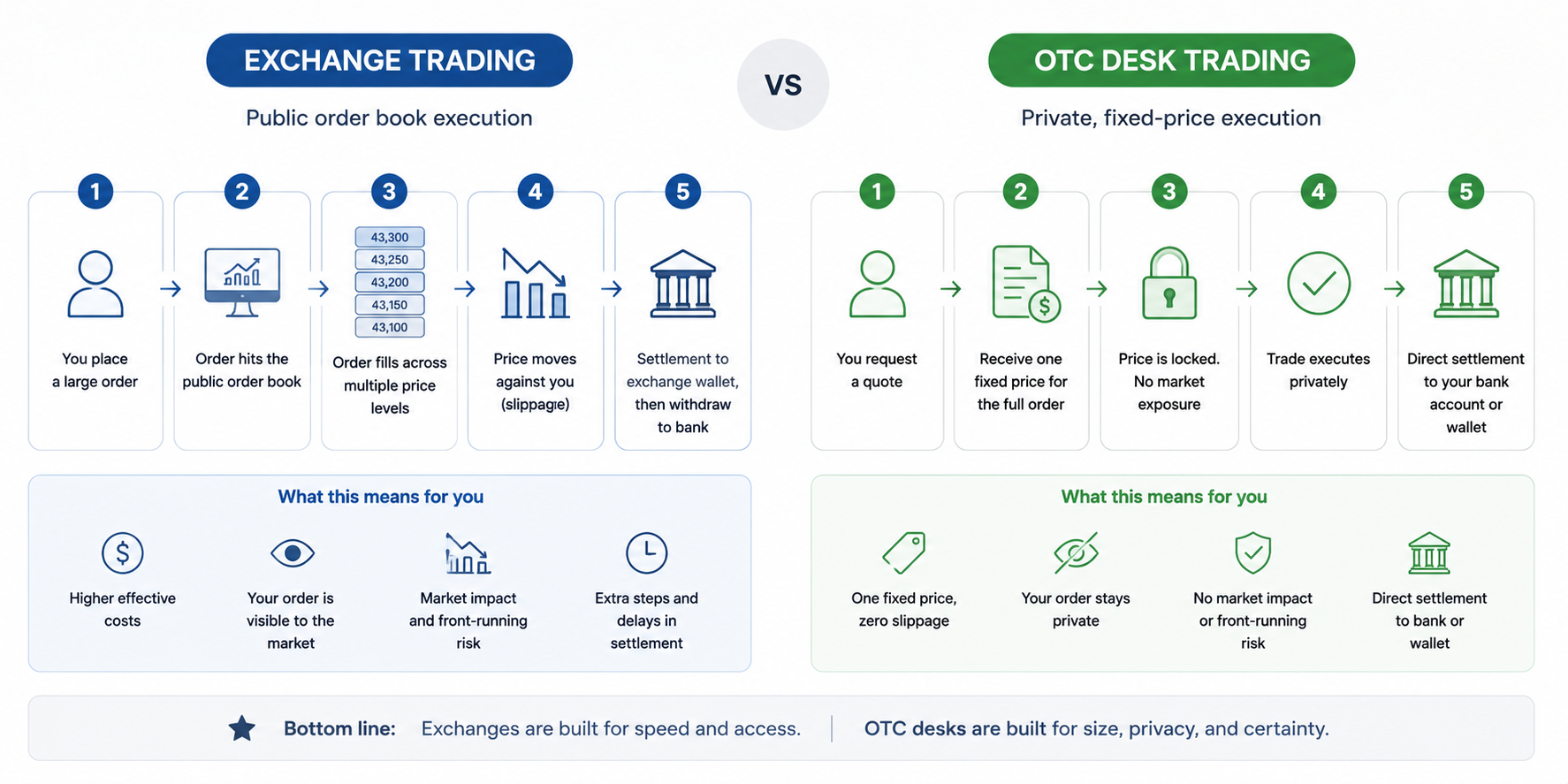

A crypto exchange is a centralized platform where buyers and sellers are matched through a public order book. Every order is visible to all market participants, prices are set by real-time supply and demand, and trades fill against whatever liquidity is available at each price level, often across dozens of price points simultaneously.

Exchange-traded assets are standardized: the same pairs, the same settlement mechanism, and the same fee structure for every participant.

On an OTC desk, the order book is removed entirely. Instead of trading against anonymous market participants at multiple price levels, you trade directly with a counterparty at a single agreed price for the full order. OTC trades can be customized in ways exchanges cannot accommodate: settlement timing, destination currency, and bank account routing are all configurable.

The trade is private, the price is fixed before execution begins, and proceeds settle directly to your verified bank account or whitelisted wallet.

Unlike exchange prices, which are set by real-time supply and demand, OTC prices are quoted by the desk based on current market conditions, available liquidity, and order size. The desk builds its margin into the spread rather than charging a separate commission.

To understand the full mechanics of the OTC desk model, read our guide on what is an OTC desk.

The core distinction between OTC and order-book crypto execution is simple: one model walks the book at progressively worse prices; the other agrees to a single price before anything moves.

A $500,000 BTC sell order on a public exchange does not fill at one price. It fills against buy orders sitting at different levels across the book: the first $100,000 at $43,200, the next $150,000 at $43,050, and the remainder at $42,800. By the time the order completes, the average execution price is meaningfully below the rate shown when the trade was placed. That gap is slippage, and it compounds directly with order size.

For a treasury team executing this trade weekly, the cumulative cost across a year is significant and entirely avoidable through OTC trading.

On a crypto OTC desk, you request a quote for the full $500,000. The desk responds with a single fixed price for the entire amount, reflecting current liquidity conditions and its spread. You accept or decline. If you accept, the trade executes at that price regardless of market movement during settlement. The order never touches the public book, produces no visible price signal, and causes no market impact on the exchanges' other participants.

When evaluating OTC trading vs. exchange, the practical differences across pricing, settlement, privacy, and support come down to eight specific factors.

The settlement flexibility row carries more weight than it might appear. OTC desks can accommodate specific timing requirements, multi-currency settlement, and direct bank account routing. These are structural capabilities that no exchange can replicate regardless of trade size or account tier.

Not every trade belongs on an OTC desk, and a well-calibrated institutional operation uses both models for what each does well. Exchange trading is the right execution method in these situations:

According to Finery Markets' 2026 institutional OTC report, 40% of surveyed institutions now name OTC as their first-choice execution venue, routing more than half of all their digital asset trades off public exchanges. The question of should institutions use an OTC desk comes down to four specific triggers:

OTC and exchange markets serve distinct roles in the crypto market structure. Exchanges provide the price discovery and liquidity backbone that retail markets depend on. OTC desks absorb large institutional flow privately, reducing the market impact those trades would otherwise cause on public order books. Getting the allocation right between crypto OTC vs. exchange trading is what separates reactive execution from deliberate institutional market structure.

For institutions evaluating crypto OTC vs. exchange trading in the MENA region, Fuze Finance is VARA-regulated, SOC 2 Type II- and ISO 27001-certified, and purpose-built for institutional volume. The desk processes over $4 billion in annual volume across more than 400 onboarded institutions and supports over 100 digital assets, including BTC, ETH, SOL, USDC, and USDT.

Every quote is locked for 10 seconds through an RFQ system, among the highest price lock windows in the industry, and is all-inclusive with fees and taxes built in and nothing added after acceptance. Settlement runs on T+0 for all major tokens, with direct fiat proceeds available in AED, USD, EUR, GBP, and TRY. Every client is assigned a dedicated relationship manager available round the clock.

%20(1)%20(1).png)